- News |

-

- Featured

-

Canada’s privacy commissioner launches investigation over the use..

As the years pass by, technology also widens, and more and more are being discovered. From simple gadgets..

- Business |

-

- Featured

-

Be an informer to I-T dept; earn up..

Sharing "specific information" with the income tax department about any benami..

- Tech & Industry |

-

- Featured

-

Gravitational wave event likely signaled birth of black..

The merger of two neutron stars that generated gravitational waves detected last year may have led to the birth..

- Entertainment |

-

- Topics

- Malayalam Film

- Media

- Music

- Youth

-

- Featured

-

Shawn Mendes Released Highly Anticipated Self-Titled Album Today

Los Angeles, CA : Multi-Platinum singer/songwriter Shawn Mendes released his highly anticipated self-titled third album today, via Island Records. Get..

-

- New Products |

-

- Topics

- General

-

- Featured

-

ZOTAC Introduces Its GeForce GTX 960 series graphics..

Dubai- ZOTAC International, a leading innovator and manufacturer of graphic cards and mini-

-

- Education |

-

- Topics

- Campus News

-

- Featured

-

ITM University, Gurgaon Student Palash Chhabra Represents Varsity..

New Delhi: Palash Chhabra, a student of ITM University,..

-

- Health |

-

- Topics

- Medical News

-

- Featured

-

Maharshi Shushruta, The Great Grandfather of Surgery!

by Ayurvedacharya Dr.Hitesh Jani Dr.Hitesh Jani

-

- Tourism |

-

- Topics

- Travel

- Food&Beverages

- Hospitality

-

- Featured

-

“Keraliya Ayurveda is Credible and Authentic”

Irina Gurjeva Irina Gurjeva is not just another vacationer in..

-

- Sports |

- Editor's column |

- Magazine |

ICRA maintains stable year-end outlook for Construction sector

Published on December 24, 2019

ICRA has given a stable outlook for the construction sector, in its year-end assessment of the sector.

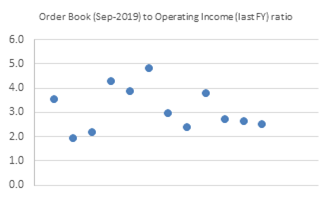

The order inflow for construction sector has been robust over the last few years, supported largely by increased Government spending towards infrastructure. However, H1-FY2020, has witnessed lower new order inflows and cancellations of some orders in the state of Andhra Pradesh, which has resulted in a decline in order book for some players. Nevertheless, the order-book position of most of the construction players is currently adequate to provide medium term revenue visibility.

As the Government plans to more than double the investment in Infrastructure to about Rs. 100 trillion over the next five years, the construction companies are likely to witness significant opportunities with key segments being highways, railways, ports, urban infrastructure and airport. In the Railways segment, besides the core railway capex (doubling, new lines, signalling, electrification, etc), the station redevelopment, is expected to provide significant opportunities to the construction companies. Similarly, in the highways sector, adequate pipeline of projects for development/upgradation of the national highways and state highways exists. The Bharatmala Pariyojana project itself is expected to provide large opportunities for the construction sector as the programme is the largest road development programme in India.

With a huge pipeline of projects to be awarded in the infrastructure sector, ICRA expects the new order inflows for construction companies to improve in CY2020. However, delays in land acquisition, funding issues, and State Government priorities remains key risks to the new order inflows. The order inflows from non-infrastructure segments like industrial and real estate (excluding affordable housing segment) is expected to remain muted, with weak private sector capex growth.

On the execution front, ICRA expects the healthy order-book should support growth in operating income of construction companies in the first half of CY2020, though it could witness moderation if the new order inflows weaken. However, construction companies which have leveraged balance sheets and stalled or slow-moving projects, would continue to face challenges.

As for financial health, operating profitability is expected to remain stable with the benefits of benign inflation and steady execution; though this would also be dependent on any steep variation in key raw-material and labour cost. However, the capex and working capital requirement could absorb most of the cash accruals. The working capital cycle for the larger construction players has remained at higher level, owing to slow realization of receivables, and slow-moving legacy projects. This has been met partly by higher creditors, thus percolating to sub-contractor’s working capital cycle as well. The working capital situation is not likely to see any major improvement in the near term. Further, many construction entities have faced challenges in meeting their Bank Guarantee requirement which is likely to persist. In the absence of adequate Bank Guarantee limits, companies will not be able to unlock retention money or avail mobilization advances thereby having an adverse impact on their liquidity.

With healthy accruals, the balance sheet of many construction companies has improved over last 2-3 years. With increased scale of operations, the debt of construction companies is expected to increase, albeit marginally, except in the case of increase in working capital intensity or investment in asset owning model like the Hybrid Annuity Model (HAM) based projects where the increase in borrowing could be higher. While the overall credit profile of construction companies has improved in last couple of years, many players in the sector still remain highly leveraged and their liquidity pressure is likely to persist in the short-term as the lenders remain cautious towards the infrastructure/construction sectors. Their ability to raise funds via stake sale in its subsidiaries, monetisation of assets, or dilution of equity will be key factors in improving liquidity and the capital structure, particularly for companies that have been aggressive in the BOT space in the past.

Asset monetization can also help in lowering the borrowing levels for companies which have operational assets. Many such transaction have taken place in the last few years particularly in the road sector, with active interest from private equity, pension funds, and other long-term investors in acquiring operational projects. Infrastructure Investment Trust (InvIT) can also help lowering the leverage for construction companies which had ventured into asset-owning business and have multiple operational projects. With an improvement in the equity capital markets, equity-raising ability has also improved. Some construction companies have successfully raised funds through the equity route like IPO/QIPs/rights issue/warrants/preference shares, which has helped in improving their balance sheet and liquidity position.

Due to these factors, ICRA expects the credit profile of construction companies to remain stable in the short to medium term