- News |

-

- Featured

-

Canada’s privacy commissioner launches investigation over the use..

As the years pass by, technology also widens, and more and more are being discovered. From simple gadgets..

- Business |

-

- Featured

-

Be an informer to I-T dept; earn up..

Sharing "specific information" with the income tax department about any benami..

- Tech & Industry |

-

- Featured

-

Gravitational wave event likely signaled birth of black..

The merger of two neutron stars that generated gravitational waves detected last year may have led to the birth..

- Entertainment |

-

- Topics

- Malayalam Film

- Media

- Music

- Youth

-

- Featured

-

Shawn Mendes Released Highly Anticipated Self-Titled Album Today

Los Angeles, CA : Multi-Platinum singer/songwriter Shawn Mendes released his highly anticipated self-titled third album today, via Island Records. Get..

-

- New Products |

-

- Topics

- General

-

- Featured

-

ZOTAC Introduces Its GeForce GTX 960 series graphics..

Dubai- ZOTAC International, a leading innovator and manufacturer of graphic cards and mini-

-

- Education |

-

- Topics

- Campus News

-

- Featured

-

ITM University, Gurgaon Student Palash Chhabra Represents Varsity..

New Delhi: Palash Chhabra, a student of ITM University,..

-

- Health |

-

- Topics

- Medical News

-

- Featured

-

Maharshi Shushruta, The Great Grandfather of Surgery!

by Ayurvedacharya Dr.Hitesh Jani Dr.Hitesh Jani

-

- Tourism |

-

- Topics

- Travel

- Food&Beverages

- Hospitality

-

- Featured

-

“Keraliya Ayurveda is Credible and Authentic”

Irina Gurjeva Irina Gurjeva is not just another vacationer in..

-

- Sports |

- Editor's column |

- Magazine |

NeighborWorks Housing Solutions Announces Emily Simpson as Resource Development Associate

Real Estate to witness positive demand revival; market fundamentals continue to remain strong

Published on October 21, 2021

Fast tracking tech adoption, sustainability measures to be agents of change for the real estate sector

Mumbai: Confederation of Indian Industry (CII) in association with JLL as knowledge partner today organized the 13th Edition of CII Realty & Infrastructure Conclave 2021. Themed as “What’s next: The future of real estate,” the event, a virtual thought leadership forum is attended by the country’s top real estate professionals. This conclave has been one of India’s leading platforms for experts to discuss opportunities, share insights and predict the course for the industry for over a decade.

The conclave saw the launch of the CII-JLL research report titled ‘The Future of Indian Real Estate: Charting new growth in times of new realities”. The CII-JLL report provides a comprehensive analysis on the future of Indian real estate.

Radha Dhir, Chairperson, CII Realty & Infrastructure Conclave, CEO & Country Head, India, JLL, said, “The pandemic did halt much of the industry’s growth, however there are lots of green shoots emerging and transforming the future of all asset classes with multi-fold opportunities. Today, real estate has come to the centre of the board discussions and is redefining business growth strategies. Commercial real estate has shown resiliency in 2021 and is likely to gain momentum in 2022. The office will continue to remain the centre of the work ecosystem to reinforce culture, drive collaboration and innovation, enabling professional growth and bring the best brand experience to clients and employees. The residential market remains on track to recover completely to pre- COVID levels.” “Structural changes such as an increasing middle class, accelerating e-commerce, technological innovations and advancements in sustainable solutions are propelling the demand for logistics and industrial growth. Non-traditional forms of real estate assets like data centers, healthcare, life sciences educational institutions, senior living, co – living and student housing–have become increasingly popular. Macroeconomic drivers such as urban growth, adoption of Internet and smart phones, and an aging population underpin the need for these alternative assets,” she further added.

Office market resilient in 2021, growth shoots in 2022 and beyond

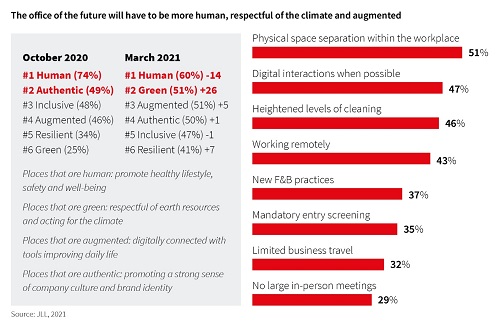

The office of the future will have to be more human, respectful of the climate and augmented. While the sector has witnessed better activity in the commercial office segment, it is likely to end on a lower to flat net absorption level compared to 2020, signifying the headwinds that impacted the segment this year. But positive signs of occupier activity are visible amid India’s continued momentum as an outsourcing/offshoring destination. India’s REIT market will enter a period of prolonged growth, with more REITs forecast to be listed in 2021 and beyond. CII-JLL report believes that India’s office market of 653 million sq. ft as of H1 2021 across seven major cities has a potential of 280 million sq ft that could be securitised with an estimated value of USD 35 billion.

Investment momentum on track

Investments continued unabated and registered USD 2,668 million during H1 2021, which was three times the H1 2020 period. The first half of 2021 saw broader participation with 26 deals as against 14 deals Year-on-Year (Y-o-Y). “The lockdown relaxations during the first quarter of 2021 provided a first-hand glimpse and experience of a post-pandemic world to investors, which led to re-rating. of risks with asset allocation witnessing a change during H1 2021. Investors have come to accept that they must operate in an environment of constraints and some uncertainty Another silver lining during the pandemic period was the successful debut of two listed REITs with good responses from retail as well as the institutional investor segment. The success of the first REIT listing of Embassy REIT in April 2019 provided a good start for the REITs market in India,” Dr. Samantak Das, Chief Economist and Head Research and REIS, India, JLL.

Affordable synergies’ and ‘home ownership’ to push growth in the residential sector

The development focus on the affordable and mid-price segment is expected to continue. Over the next one year, it is expected that new launches will remain concentrated in affordable and mid-price segment with developers trying to reap the benefits of strong pent-up demand and government incentives in this segment.

Sustainability gaining importance in residential developments

COVID-19 has shown how important sustainability is for the future. It has given us an opportunity to ensure that we increase resiliency through sustainable policies and practices. A lot of residential developers in India are also taking conscious efforts to adopt eco-friendly and sustainable building practices. India’s real estate sector (particularly the commercial and residential asset classes) accounts for over 33% of energy consumption in the country and this share will likely touch near 40% by 2025. The need of the hour is to further accelerate this wave of green transformation and facilitate a greener and healthier built environment. The pandemic has shifted the focus towards health and wellbeing aspects apart from providing the amenities and facilities in residential projects. Well-executed green residential developments perform extremely well financially, as they require lower operating costs, increase health and productivity of the occupants, and have higher marketability.

Flex spaces gathering steam post a rationalization during the pandemic

Flex operators are looking at back-to-back deals, where they sign a space as a managed space provider for an occupier with immediate needs. Most of the growth is coming from such managed space providers who are catering to space needs for large enterprises. Unlike earlier, where occupier needs for a managed space were largely of an interim nature, occupiers are willing to make long-term commitments for such spaces. Approximately 31,000 flex seats were leased till H1 2021, which is already 90% of the total seats leased by corporates in flex spaces. 0.7 million sq ft has been leased by flex operators in H1 2021 which is compared to 2.9 million sq ft that was leased by flex operators in 2020. The flex stock in top seven cities at circa ~30 million sq ft. continued to hold steady through the COVID period

Evolving workplace: Hybrid model is here to stay

In the current environment, the discussion has shifted from buildings and workspaces to the workers and workplace experience. Companies would be amiss to not pay heed to what their

workforce demands and shaping their workplace strategies to a more worker-oriented one is the way forward as they look to bring their workers back to offices.

As part of a JLL Global Workers Performance Barometer report to understand how office workers feel about their homeworking and how it impacts their priorities at work, performance and well-being, some interesting results were visible.

Graphical user interface Description automatically generated

In what JLL termed as the ‘ratchet’ effect of the pandemic, workers are now prioritizing an empathetic employer and work-life balance over salary. In fact, over 53% of all respondents in India, put a caring employer concerned with their health and well- being as their number one priority in the latest survey findings of March-April 2021 (it was the third in priorities in the October 2020 survey). As workers aspired for more balanced working patterns, it has become imperative for employers to realign their strategies to a more hybrid and inclusive model.

Realty market: Charting new growth in times of new realities

Despite the setback of the pandemic, market activity in the real estate sector is recovering, though a more sustained recovery is needed to tide over the shocks of the past 18 months or so. While there will be continuation of better activity in the commercial office segment, most likely 2021 will close on a lower to flat net absorption level compared to 2020, signifying the headwinds that impacted the segment this year. The country’s rise on the back-office outsourcing/offshoring value chain has now firmly established it as a destination of choice for corporates looking for cost-effectiveness as well as a diverse talent pool to harness their R&D and innovation strategies.

With the recovery in the residential segment looking quite secure given the benign interest rates and affordability synergies supporting demand improvement, structural reforms continue to be the bedrock on which the segment is gaining new strength.